Are you ready for increased employee choices and flexibility in the workplace?

There is no doubt that we are all living through an exceptional period of time, as a result of the pandemic. We have seen a revolutionary and practically overnight shift from office-based work to international remote home working that became a necessity, as governments sought to control the spread of the virus.

This ‘new normal’ has come with lifestyle benefits for employees such as reduced costs of commuting, more time for personal development and a better work-life balance. Many employees have adapted successfully and would prefer to, at least part-time, continue working remotely after the pandemic. Business leaders, too, have embraced this ‘new normal’ and are more comfortable with the benefits of the shift to remote working, which include costs savings from reduced business travel and office space.

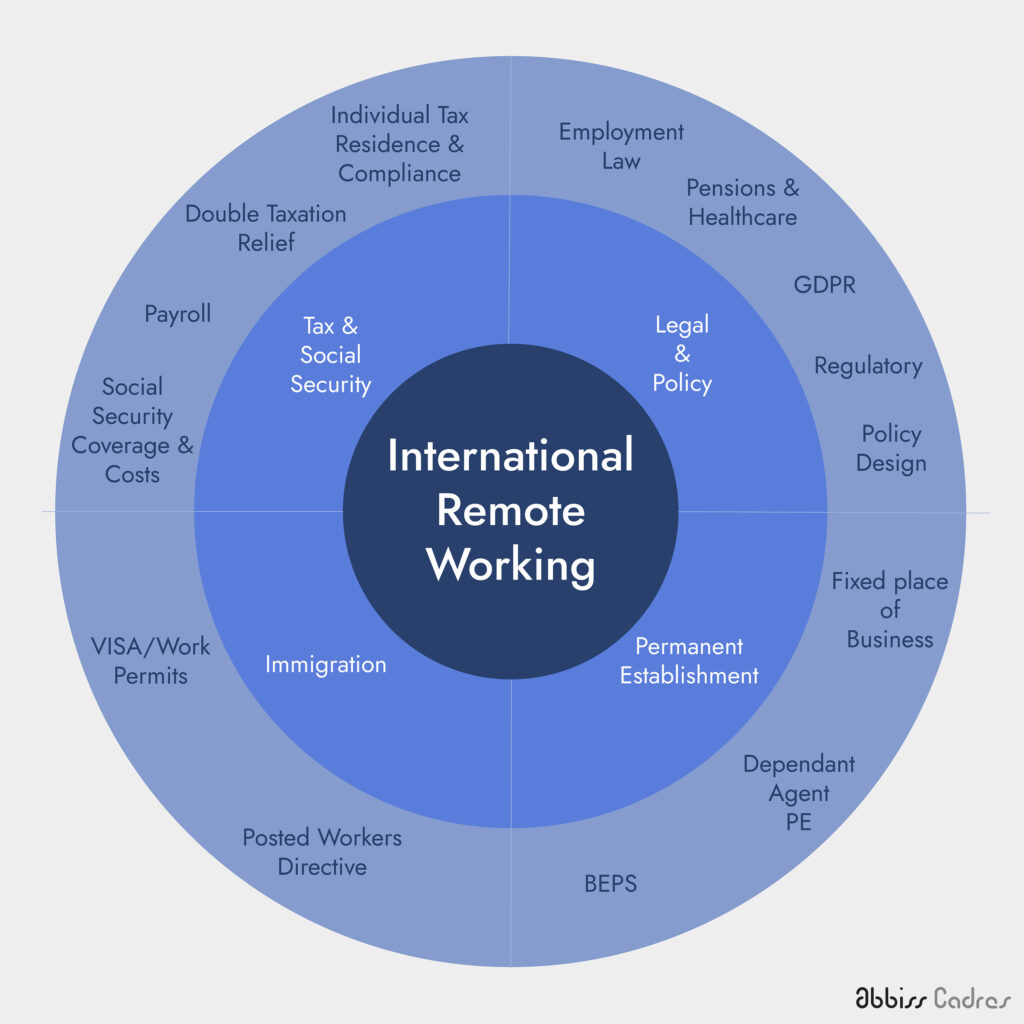

For business, one area that is emerging is the compliance challenge of international remote working, where employees working from ‘home’ may mean working in another country for an extended period of time. Although this may create challenges in the short-term, these are not insurmountable and should not be a barrier to future international remote working.

At the start of the pandemic, it was almost impossible for any business travel to happen. Many employees posted or employed abroad returned to their home countries with the intention of working there temporarily until travel restrictions were lifted. These temporary dislocations led to initial tax and social security questions around where taxes should be paid for the work being performed. Governments announced easements to avoid some of the unintended consequences and we covered examples of these in our previous article.

With continued restrictions, temporary displacements have become more permanent. The ‘home’ where the employee is working from is no longer necessarily the country of employment, and therefore the location of where the duties would have been performed has changed. This shift can also impact the tax and social security position as well as employment law rights and employer obligations.

HR teams are starting to grapple with complex legal, tax, social security, payroll and immigration challenges that are arising. Many of these do not manifest or become obvious in real-time, especially in the uncertain times we find ourselves in. Unfortunately, this does need addressing to avoid unexpected and costly outcomes.

The key areas of consideration

Tax and Social Security

As a result of the pandemic, international remote working has resulted in the following scenarios:

- Some assignees returning to their ‘home’ country to work remotely

- International commuters no longer commuting

- Individuals employed one country returning to their country of nationality, where the employer does not have a presence

- Board meetings taking place remotely

- New hires who are unable to relocate to a new country to start a new role

All of these changes to working may impact where the employee is classified as a resident and liable to tax. As a result, tax and social security may be withheld and reported in the wrong country. For example, for someone working cross-border, tax withholdings that take account of their work patterns are usually agreed with tax authorities in advance and have continued to be applied during the current tax year. For displaced workers, this can lead to tax adjustments being required when completing tax returns after the end of the tax year. It can also lead to common cash-flow issues, such as where a tax liability becomes due in the ‘home’ country before a repayment can be claimed from the country where the tax is withheld. Employees faced with such an outcome are likely to be looking for support from their employer.

The compliance aspects are not just restricted to individuals’ tax return compliance. There is also a responsibility for employers to account for tax and social security withholdings. In some circumstances, social security may become due in the ‘home’ country, and this may be accompanied by the need for employers to register and account for employer social security costs that have not been budgeted for.

Legal and Policy Matters

Employment contracts will typically set out where the employee is required to work. Flexible arrangements such as working from home may be informally or formally agreed between the employer and employee. During the pandemic, governments required employees to work from ‘home’ where possible and employers supported their employees to do this. As highlighted earlier, in some instances, the ‘home’ is not in the country of employment. This does result in a number of legal and policy aspects that employers need to consider in order to formalise any international remote working arrangements.

Employment law

In the area of employment rights, most countries have mandatory provisions that apply as long as the worker is physically located within the jurisdiction, regardless of the law applicable to the contract. While a short period abroad for an employee, normally, might not have any effect on employment rights, longer periods that have become essentially open-ended as a result of pandemic-related travel restrictions. This may mean that HR teams will have to consider not just one but two or possibly more sets of employment laws, covering areas such as dismissal rights, health and safety, health care and pension benefits. There may also be regulatory consequences of long-term remote working.

Securities law

The grant of share options, and other forms of incentives using equity or other securities, may be subject to restrictions under the securities laws of the jurisdiction where the recipient lives. When making such awards to employees, the implications of securities laws must be considered in each jurisdiction where the offer of shares or other securities is made.

Allowing employees to work from a variety of different jurisdictions will inevitably increase the number of different security regimes that must be checked by the company granting the awards. However, it is essential that companies follow through with this, as failure to comply with the requirements of a securities regime may, in some circumstances, constitute a criminal offence. In addition to the risk of any penalties for non-compliance (which may, in practice, be low), there is a reputational risk for a non-compliant company of being seen to operate in disregard of local law.

Data protection issues for employers with employees Working from Home

In a new business environment where most staff are working from home, employers will now, more than ever, need to be aware of potential data protection issues. Part of an employer’s obligations under GDPR and the UK Data Protection Act 2018 is to document and demonstrate compliance of the legislation.

Employers need to be wary of their employees transferring data either abroad or from abroad. For example, if an employee’s role involves processing either personal data or sensitive personal data (such as data around an individual’s race/ethnicity, political opinions, religious/philosophical beliefs, trade union membership, genetics, biometrics, sex life/sexual orientation, or health) and the employee is currently displaced in a country outside of the EEA, additional restrictions around transferring such data apply. We would recommend employers seek legal advice, as the rules in this area can be complex.

Immigration

Anyone in the UK who had leave to remain expiring between 24 January 2020 and 31 July 2020 could have requested to have their visa extended until 31 July 2020 if they could not return home owing to travel restrictions and a further grace period was added up to 31 August 2020. Following that it was necessary to apply for an “exceptional assurance” to guard against adverse action or consequences after the leave to remain expired. This remains the case during the current national lockdown and the guidance extends the period until 31 January 2021, although it is likely to be extended further.

Anyone currently in the UK who cannot travel owing to COVID-19 can apply to switch to another category. This includes applications where you would usually need to apply for a visa from your home country. This includes people whose leave to remain ends up to 30 November 2020.

If your visa or leave expired between 24 January 2020 and 31 August 2020, there will be no future adverse immigration consequences if you didn’t make an application to regularise your stay during this period. However, if you have not applied to regularise your stay or submitted a request for an exceptional assurance you must make arrangements to leave the UK.

If individuals have made or are making an application and cannot currently book appointments because application, service and support centres are temporarily closed owing to COVID-19, then people who have made appointments will be contacted and told when they can make new ones.

Where a Certificate of Sponsorship (CoS) has been issued to an employee but they have not yet been able to apply for a visa, they may still be able to start work once the application is made and before a decision is given. The start date for employment stated on the CoS may have changed. The Home Office will not automatically refuse such cases. For example, they may accept a CoS if they have become invalid because the employee was unable to travel as a result of Coronavirus. The Home Office will consider this on a case-by-case basis.

Permanent Establishment

Where an employee works from home, their activities should also be monitored, as they can create a corporate presence or a permanent establishment in the country where work is performed. This could trigger new filing requirements and tax obligations for the employer. What constitutes a presence varies by country. Although governments have been encouraged by the OECD to consider the temporary and exceptional change of location, for ongoing scenarios, the risk will need to be considered as there is currently no uniform approach.

How should HR functions approach International Remote Working?

There is clearly much to ponder. First of all, there will be a need to identify impacted individuals for 2020 and ensure that the business meets its compliance obligations and supports individuals to meet theirs. We expect there are likely to be some surprising and unintended outcomes as a result.

This should also help the business identify some key areas of risk going forward that will help decide what may be viable and supported in the future, helping shape recruitment and retention policies as well as track processes.

What about the post-pandemic world?

Much has and will be learned from 2020. There is no doubt that the pace of change has dramatically accelerated. Now that remote working has been embraced and its benefits more clearly understood, we can see its potential evolution:

- In order to be competitive, employers may seek to access a broader global talent pool and offer employment to international remote workers.

- Some future international assignments may look different, with some changing from the traditional ‘home’ to ‘host’ relocations or virtual assignments. An assignment is where an employee will remain working remotely from the ‘home’ country for most of the time and visit the ‘host’ country from time to time for focused and necessary visits.

Providing future flexibility for employees will be attractive. While compliance risks and associated costs will always exist and need to be managed, some cost savings may ultimately be achieved in both hiring costs and less usage of traditional expensive relocation packages such as tax equalisation. Awareness of the employment regimes, where remote working employees may be located, will be key in ensuring that those cost savings are not lost by inadvertent mistakes.

How Abbiss Cadres can help?

We offer a unique combination of integrated expertise including regulated Law and Tax services, People Consulting and Communications, both in the UK and internationally. We are happy to support you with all of the issues relating to international remote working. Please get in touch to discuss how we can help your business.

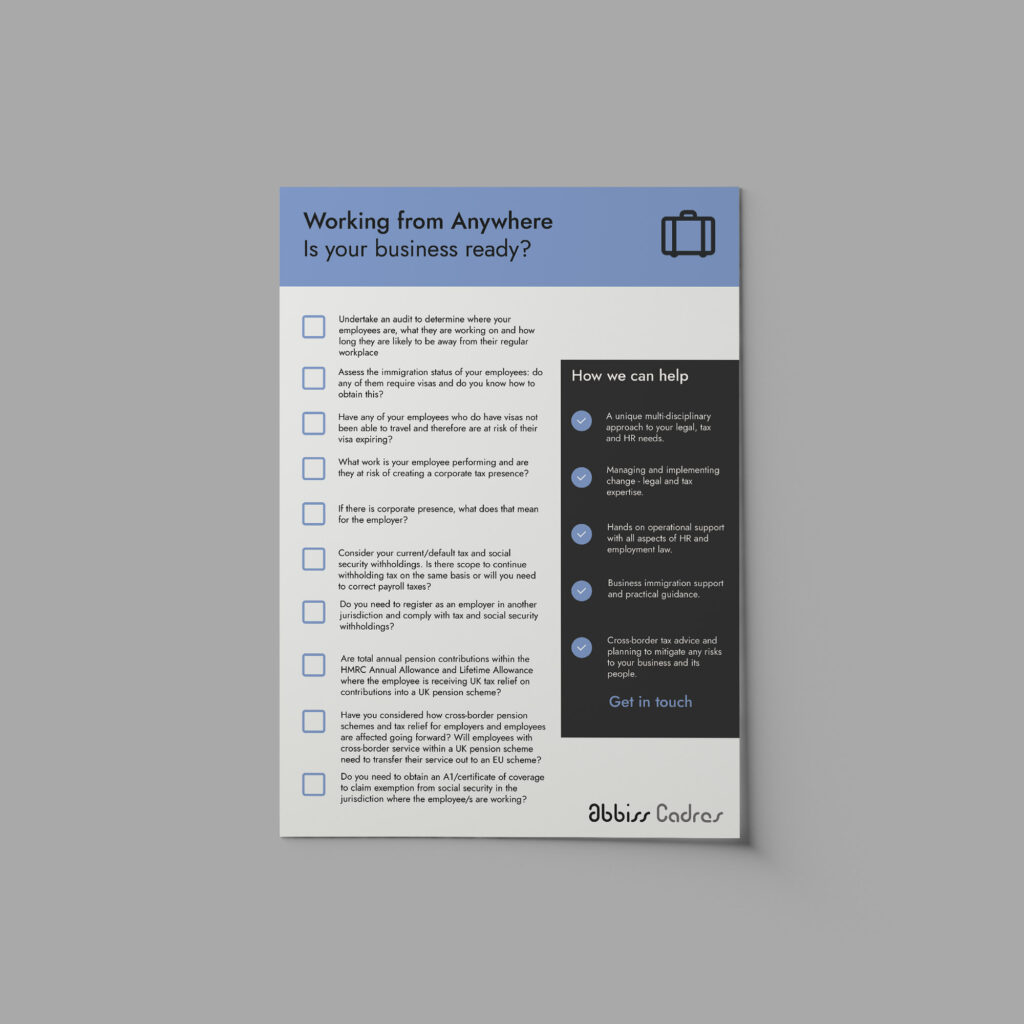

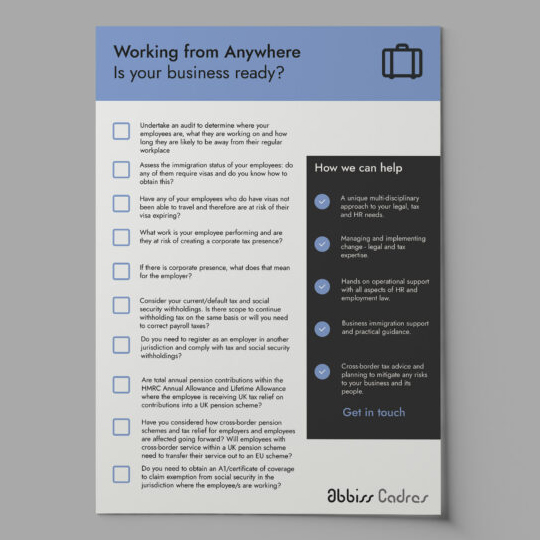

You can download our checklist of key considerations for businesses to take into account when considering international remote working, cross-border workers and global mobility by clicking on the image below.